Let’s explore the different parts of your accounting system, how all the pieces come together and how you can design an accounting system to best fit your business. Often in the process of wanting a more “robust” accounting system or wanting specific Key Performance Indicators/reports, business owners can look at different solutions to receive the financial information they desire.

| Primary Outcomes of Accounting System | Components of Accounting System | Best Practices |

| Monitor Cash In and Out | Pricing & estimating | Don’t put the cart before the horse! |

| Audit Trail & Internal Controls | Parts/Inventory | Avoid the data monster! |

| Receive Monthly Financial Statements | A/R, Billing | Do the benefits of info outweigh the costs of measurement? |

| Receive KPIs – Managerial and Financial Accounting KPIs | A/P Billing | What is the outcome?

Why am I measuring it? |

| Taxes: Planning, Estimates, and Preparation | Financial Accounting/Statements | Will I make a different business decision based on this info? |

| CRM/Scheduling | Is the info understandable and verifiable? |

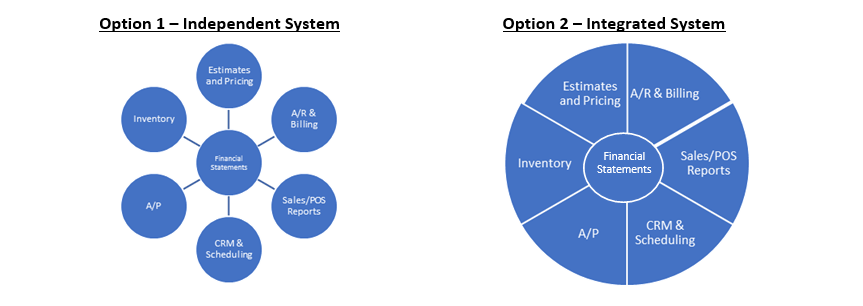

Accounting Systems: 2 Models of Operation

There are 2 models for how the potential components of an accounting system come together:

- Option 1: You have different components of your accounting system, each having a specific purpose to fulfill one part of the accounting system’s needs. Each operates independently of the other and comes together in the middle.

- Option 2: All parts of the accounting software are part of an integrated software package, and numbers transfer over from that part of the system.

All systems are one of these models which you also see visually below. A system could also be a hybrid of the two where some features might be part of one whole system, and others operate independently.

Option 1 is where the Financial Statements are created in one software program and the other pieces you see are separate components/applications/software/ or reports. Those key numbers and reports are used to prepare the financial statement however all the components are not in one software package. The key here is they are separate components and the key numbers from the outside reports are then carried over to the financial statement.

The other model, Option 2, is where all the components of your accounting system are part of one, integrated, “robust system.” You will typically find this with industry-specific software. The only difference here is all parts of the accounting system, in addition to the financial statement part as you can see in the visual above, are all housed within the same software. Each has its own part(s) within the same system- with each part making up the whole.

Organizing Principles for Best Practices

Both systems will have the same result/numbers if utilized properly. The following organizing principles are important in guiding how you design your accounting and operational cash flow systems.

- What is the outcome, and why am I measuring this? Or what outcome am looking for this information to support?

What numbers do I need, where am I getting them from, and what am I using them for?

- Do the benefits of the information received outweigh the cost of putting it together?

- There is time, energy, and dollars involved in tracking and measuring something.

- Will you make a different business decision based on this information?

- How can I measure efficiently? What information really matters?

- Is the Information understandable, and verifiable?

- Just because it is in a computer doesn’t mean all the numbers or details are pulling correctly!

- Do you understand the data the reports are giving you? Verify/follow the reports mathematically?

Clarify and verify the info in the system is correct for accuracy and reliability.

- Remember, garbage in, garbage out!

- Avoid the Data Monster! Don’t automate to the point of complexity!

Sometimes we get so lost in the numbers we forget to see the big picture (getting stuck in the trees you can’t see the forest). This can happen multiple ways with your numbers.

- Don’t put the cart before the horse! Know what numbers you need, first.

- Sometimes owners want these high-tech KPI dashboards, and they’re not tracking Cash In and Cash Out every month, or receiving a financial statement.

- And while there are some managerial accounting KPIs, they still need the most important KPIs that impact sales, profit, and cash flow that are reflected on the financial statements, which properly account for all cash in and out, sales, and expenses. Without that outcome, things will be missed, leaving out the most primary outcome needed from an accounting system, and worse yet you’re left with incomplete and inaccurate data.

- Internal Controls and Segregation of Duties for Best Practices

- Keep in mind the person paying the bills should be the one doing the bank reconciliation.

- The person doing the bills, shouldn’t also be doing the Accounts Payable

- Therefore, the accounting system has its independent parts. So, the person paying the bills doesn’t have access to the Accounts Receivable, and vice versa. Or, the person entering the bills, doesn’t have access to the accounting software that does the Bank Reconciliation. Or, the person ringing up Sales in the POS system, isn’t in charge of deposits or has access to other parts of the system. For some of these reasons, parts must meet in the middle instead of being interconnected.

Putting the Pieces Together

Let’s look at the parts of an accounting system whether it’s an independent system or an integrated system.

- A/R, Invoicing, and Collections

What matters the most: A/R Aging, Reports by Customer, and bottom-line Accounts Receivable numbers?

Whether it’s a separate A/R billing system or it’s in your accounting system, it’s the ending A/R number that goes on the financial, regardless of where you get it from.

Typically, this is part of the accounting software, but sometimes a business still has a need for this being its own separate software. For example, at many bigger accounting firms, their client count and invoice volume are so high, A/R billing needs to be an independent function within the firm, separate from Payables and other accounting functions.

What will you use to keep track of Accounts Receivable and Invoicing?

The most important thing at the end of the month is what is your Ending Accounts Receivable. That is the number that shows up on the financial statement. If you need A/R Aging, you can easily go to that report, not the financial statement. Though the financial statement has A/R on it, that can easily be adjusted whether the A/R is in the accounting software or a separate program.

- Sales/Point of Sales (POS) Reports

What matters most: Tracking sales, deposits, and making sure all the money/funds hit the bank

Whether the Sales/POS reports are in your accounting software, that information will be handled the same way at the end of the month making sure Sales and Cash coming in from Sales are accounted for.

Sales/POS Reports are sometimes apart or separate from the Accounting. What matters is the correct sales number and sales categories for the financial statements. That is what drives the sales and accounting for incoming cash. Once that is done, we have the correct numbers on the financial statement. Sales and deposits are key but not necessarily if those detailed Sales/POS reports are out of the accounting software. The POS and Sales Reports can have key managerial accounting KPIs like the average sales ticket, average guest order, and total customers for the day or week. Those managerial accounting KPIs are different than financial accounting: total sales, total cash sales, and total credit card sales.

What key numbers do you really need, and what will best support you in the tracking of sales and deposits, allowing for the key managerial KPIs?

- Estimating/Pricing

What matters most: How will you determine the pricing of your jobs, quotes, or proposals?

Whether you’re pricing or estimating is linked to your A/R or Sales system, or they’re two independent parts of the process, the Sales cost goes over to billing and becomes part of Accounts Receivable.

If you plan on comparing the estimates to what was billed, you must do those comparisons whether both of those pieces of information are in your accounting system or not. To analyze that you may have to extract certain information and put it into an Excel spreadsheet. The most common reason this may be part of the accounting software or an independent billing software is because of parts and inventory, discussed in the next section.

Are you doing estimating/pricing?

- This can be helpful if it is in your accounting system, but not necessary.

- Once you estimate something, the next step is invoicing, and then collections. All are three separate steps of the process. When you need to look back at the estimate you can go back to your software system to refer to it.

- A few times a year you should review your jobs for pricing information or have a regular practice after every job. You may consider this function to be part of the employee’s salary to review these. For example, in the remodeling business, sales commissions are paid on a percentage of gross profit and the comparison of the original pricing and estimating of what the job sold and cost, taking on a new level of importance within their business model.

- Parts/Inventory

What matters most:

When parts and inventory are a major part of the process, you must have a system with inventory and the billing system combined because invoices are generated off the parts and information in the system. For example, an auto repair shop has a system that gives the costs of parts and pricing tied automatically to his billing/invoices – separate from his Accounting Systems. That software gives him exactly what he needs to invoice, letting the customer know the cost of the repairs to their vehicle.

Another example is the business owner trying to keep a real-time inventory system between items arriving, them getting tagged, putting them on the floor, ringing up sales, and managing bills/payables to be entered into the accounting system. Doing all these tasks at the same time so your inventory system matches what is in the accounting system can be very hard to coordinate. Therefore, it can be difficult for many small businesses to track inventory in such a way with the level of complexity, detail, time, energy, and resources needed that go into executing that effectively. Even more so when you have different people executing different tasks of the process.

There are two methods to calculate inventory; one is efficient and effective, and the other can be very time-consuming. Either ends up with the same ending number. And again, make sure you avoid the data monster here. Do the benefits of the information you are receiving outweigh the costs and energy to measure it or should you find a more streamlined approach to measuring it? This is one area business owners can get lost in a sea of numbers and feel completely overwhelmed.

Question to consider: What is the easiest and most accurate way to get to Ending Inventory?

- Accounts Payable

What Matters Most: Ending Accounts Payable

That is the number on the financial. Whether all the A/P is kept in an envelope and an entry is made, or that is part of the accounting software. This one is very straightforward so we will leave it at that – bills are bills! And we always know this number is right. A judge made a comment in the courtroom that usually there are only two numbers you always know are right: in those situations, cash in the bank and what is owed to your vendors.

- Scheduling/CRM (Client Relationship Management)/ Additional Operational Needs

What matters most:

Some business requires certain applications for scheduling and customer relationship management (CRM). Some of can be tied to billing/invoices. For example, my dentist has a CRM/scheduling system and uses that for billing and scheduling. However, that is not the system they use for their accounting. In fact, their dental software was a great example where customized software fits the operational needs of the business well, but the bells and whistles tied to the accounting pieces were not very user-friendly or robust. They did not use its accounting features and took a different approach for that aspect of their system.

This often happens with industry specific software because the accounting functions are usually an extra feature and benefit. The programmer may be an expert on the industry but not on the financial and accounting application side of the program. Sometimes the added features are not as useful as one would always hope and additional time, energy, money and resources have to be devoted to get it to work. Sometimes worth it, sometimes not! That is where the data monster can again slip into the equation!

Question to consider: What are your needs and what systems are out there that will fit them? Have you compared the different applications enough? Features, benefits, cost, needs it meets, integration with other applications, verified functionally, easy to use to train the team, and implementation/switching systems (time, hours, wages)?

Selecting the right CRM can be one of the biggest decisions you make. Take your time. Research and make an informed and diligent decision. It may take many months to really get this decision right depending on what is all involved from consideration, budget, and implementation.

- Financial Statements and Accounting

Begin with the end in mind.

All the reports above are primarily managerial accounting reports to help you make decisions, and in between the months. The managerial accounting reports can also have one number or more on them at the end of the month that is carried over the financial statement. For example, the sales number, or sales number per category can get transferred over and entered onto the financial statement while other numbers stay purely managerial accounting in nature. The Financial Statements is then your ultimate feedback mechanism of how you did at the end of the month and the period you are reviewing. Your managerial accounting reports are independent and often are not related to the financial statements.

For example, at a restaurant, the average guest check, and customer count that day would be managerial accounting KPIs one would want. Those numbers while they would be on a KPI report of some sort, they are not on the financial statement anywhere. Unlike the total sales, or total sales from each category that would be found on the report and the financial statements. Another place this can occur is with an outside inventory system and an inventory adjustment at the end of the period or update in the A/R or A/P number on the financial statement.

What matters most:

- Bank Reconciliation (how cash comes in and out, and is accounted for)

- Check Details (all expenses), Deposit Detail (Incoming Cash), and other key reports

- Accurate and Timely Financial Statements and the story your three financial statements (Balance Sheet, Profit and Loss, and Cashflow Statement) are telling you about your business.

Question to consider:

Please read our article on how to develop a fundamentally sounds accounting systems for questions to design your accounting systems that will lead to your Monthly Financial Statements.

Summary

All these pieces are a part of one integrated system or independent parts, or some sort of a hybrid system. Either way, they are all connected – where each one ends is where the other begins. Meaning, the ending number one place is the matching number on the financial, whether it comes from an all in one ‘“robust system” or certain parts have their own specific system. Both can be advantageous. It all depends on your needs and resources (time, energy, investment) in designing your system.

Let’s reinforce the key principles in making your decisions.

- Keep is simple – what numbers do I need, and what is the primary purpose of each report? It’s when all those secondary purposes start adding up over time, and one too many editions later the data monster is born! That doesn’t mean not adding data or make enhancements. It means being extra mindful, purposeful, and intentional when doing so. Follow the principles we talked about at the beginning of this article. Over time you will learn to master this area with ease – improving each time you measure, review and repeat. Also, remember you will have to train, provide follow-up, learn and implement the system with you and your staff.

- You can automate to the point of complexity!

- And at all costs Avoid the Data Monster!

Keep in mind these are general insights and conversation points. Different industries and the size of businesses have different needs and may not even be the same from one similar business to the next, depending on the owner or business model. The discussion points are simply to help you explore how to keep your accounting systems simple. Remember, numbers can be complex but not infinitely complex and with the right structure you can streamline things to save time, money, and energy, and still give you the exact information you need to make smarter business decisions.

Please contact EWH today to discuss how you can apply these insights in to your business!